March 25, 2024—Rates Remain Fairly Steady – Forbes Advisor – Technologist

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors’ opinions or evaluations.

Today’s current average mortgage rate on a 30-year fixed mortgage is 7.37%, down 0.12 percentage point from the previous week.

Borrowers may be able to save on interest costs by going with a 15-year fixed mortgage, as they generally have a lower rate than that of a 30-year, fixed-rate home loan. The average APR on a 15-year fixed mortgage is 6.48%. But keep in mind that you’ll have higher monthly payments since you’re paying off your loan in half the time (15 years versus 30 years).

If you want to refinance your existing mortgage, check out the latest mortgage refinance rates.

Current Mortgage Rates for March 25, 2024

30-Year Mortgage Rates

Today’s 30-year mortgage—the most popular mortgage product—is 7.37%, down 0.12 percentage point from a week earlier.

The interest rate is just one fee included in your mortgage. You’ll also pay lender fees, which differ from lender to lender. Both interest rate and lender fees are captured in the annual percentage rate, or the APR. This week the APR on a 30-year fixed-rate mortgage is 7.29%. Last week, the APR was the same.

Let’s say your home loan is $100,000 and you have a 30-year, fixed-rate mortgage with the current rate of 7.37%, your monthly payment will be about $690, including principal and interest (taxes and fees not included), the Forbes Advisor mortgage calculator shows. That’s around $148,422 in total interest over the life of the loan.

15-Year Mortgage Rates

Today, the 15-year mortgage rate is 6.54%, lower than it was one day ago. Last week, it was 6.70%.

The APR on a 15-year fixed is 6.48%. It was 6.48% this time last week.

With an interest rate of 6.54%, you would pay $873 per month in principal and interest for every $100,000 borrowed. Over the life of the loan, you would pay $57,186 in total interest.

Jumbo Mortgage Rates

The current average interest rate on a 30-year, fixed-rate jumbo mortgage is 7.38%— 0.04 percentage point down from last week. The 30-year jumbo mortgage rate had a 52-week APR low of 5.00% and a 52-week high of 10.50%.

A 30-year jumbo mortgage at today’s fixed interest rate of 7.38% will cost you $691 per month in principal and interest per $100,000. On a $750,000 jumbo mortgage, the monthly principal and interest payment would be approximately $5,182.

How Much House Can I Afford?

Buying a house is a huge purchase and can put a big dent in your savings. Before you start looking, it’s important to calculate how much house you can afford and you’re willing to spend.

Not only do you want to consider your income and debt, but you also want to factor in emergency savings and any long-term financial goals such as retirement or college.

These are some basic financial factors that go into home affordability:

- Income

- Debt

- Debt-to-income ratio (DTI)

- Down payment

- Credit score

How Are Mortgage Rates Determined?

Multiple factors affect the interest rate for a mortgage, including the economy’s overall health, benchmark interest rates and borrower-specific factors.

The Federal Reserve’s rate decisions and inflation can influence rates to move higher or lower. Although the Fed raising rates doesn’t directly cause mortgage rates to rise, an increase to its benchmark interest rate makes it more expensive for banks to lend money to consumers. Conversely, rates tend to decrease during periods of rate cuts and cooling inflation.

Home buyers can make several moves to improve their finances and qualify for competitive rates. One is having a good or excellent credit score, which ranges from 670 to 850. Another is maintaining a debt-to-income (DTI) ratio below 43%, which implies less risk of being unable to afford the monthly mortgage payment.

Further, making a minimum 20% down payment can help you avoid private mortgage insurance (PMI) on conventional home loans. If you can afford the larger monthly payment, 15-year home loans have lower rates than a 30-year term.

What Is the Best Type of Mortgage Loan?

Many home buyers are eligible for several mortgage loan types. Each program can have its own advantages:

- Conventional mortgage. A conventional home loan is ideal for borrowers with good or excellent credit to qualify for competitive rates. Additionally, making a minimum 20% down payment helps you waive private mortgage insurance premiums.

- FHA loan. An FHA home loan is best when applying with imperfect credit or a low down payment. You can put as little as 3.5% down with a credit score above 580. A minimum 10% down payment is necessary for credit scores ranging from 500 to 579.

- VA loan. Borrowers with a qualifying military background may prefer a VA loan for its flexibility. A down payment may not be required. While you pay a one-time funding fee, there are no ongoing mortgage insurance premiums or service fees.

- USDA loan. Applicants in eligible rural areas can buy or build a home with no down payment, although an upfront and annual guarantee fee applies. Additionally, income requirements apply and this program requires a moderate income or lower.

- Jumbo loan. Homebuyers in a high-cost-of-living area will need to apply for a jumbo loan when the loan amount exceeds the Federal Housing Finance Agency’s conforming loan limits. The limit in most municipalities is $726,200 in 2023.

Frequently Asked Questions (FAQs)

What is a good mortgage rate?

A competitive mortgage rate currently ranges from 6% to 8% for a 30-year fixed loan. Several factors impact mortgage rates, including the repayment term, loan type and borrower’s credit score.

How to get a lower mortgage interest rate?

Comparing lenders and loan programs is an excellent start. Borrowers should also strive for a good or excellent credit score between 670 and 850 and a debt-to-income ratio of 43% or less.

Further, making a minimum down payment of 20% on conventional mortgages can help you automatically waive private mortgage insurance premiums, which increases your borrowing costs. Buying discount points or lender credits can also reduce your interest rate.

How long can you lock in a mortgage rate?

Most rate locks last 30 to 60 days and your lender may not charge a fee for this initial period. However, extending the rate lock period up to 90 or 120 days is possible, depending on your lender, but additional costs may apply.

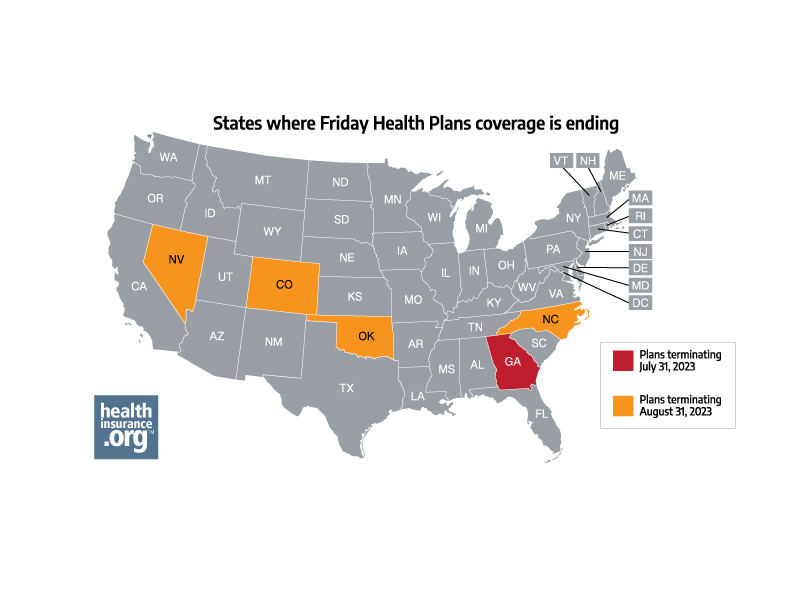

How Friday Health Plans insolvency will affect policyholders in five states – Technologist

Features, Pros & Cons – Forbes Advisor – Technologist

How to Start an E-Commerce Business In 2024 – Forbes Advisor – Technologist

About The Author

admin

Azeem Rajpoot, the author behind Technolo Gist, is a passionate tech enthusiast with a keen interest in exploring and sharing insights about the rapidly evolving world of technology. With a background in Technologist, Azeem brings a unique perspective to the blog, offering in-depth analyses, reviews, and thought-provoking articles. Committed to making technology accessible to all, Azeem strives to deliver content that not only keeps readers informed about the latest trends but also sparks curiosity and discussions. Follow Azeem on this exciting tech journey to stay updated and inspired.